seekingalpha.com

Dec 16 2013

China's Best Days Have Ended

For the past 25 years or so, China has been the benefactor of currency imbalance that made its products very cheap for US consumers and made US products very expensive for Chinese consumers. The result of this currency imbalance was a giant shift from manufacturing in the US to manufacturing in China, and the shift was gravity-like, totally unavoidable. The chart below shows the plunge in US manufacturing jobs in the US over that time on the left axis. On the right axis, we can see that Chinese exports to the US (green) grew much faster than US exports to China (red). In short, these large economic changes occurred due to a weak Chinese yuan and a strong dollar, but those days are over.

Some may ask themselves, why would the US allow China to steal all of the manufacturing growth? Some may even see the US as technically allowing itself to go bankrupt because of this, but this was allowed as a result of free trade, not ignorance. The theory of free trade is that countries that have more free trade will end up more efficient than other countries because there are more sellers to compete with. In other words, countries that use currency to improve their economies will tend to see short-term economic growth while countries which are on the other end of the stick will see long-term economic growth but short-term pain (as a direct result of forced efficiency).

Consequently, this explains why the US did not impose any meaningful trade restrictions on China. The US wanted to make things tough on itself rather than easy, to attain its goal of long-term growth.

Just how hard does the US want it on itself? All evidence suggests the hardest in the world. An example is that at the start of all of this US manufacturing meltdown, NAFTA was passed, and this forces substantial free trade all over North America. So not only is the US still at a slight pricing disadvantage with China, and most of Southeast Asia, the US has competition from Mexico and Canada without any impediments.

Because China has begun to substantially strengthen its currency towards a free market exchange rate with the US, growth in China is already slowing. It is becoming more expensive for Americans to buy Chinese products and cheaper for the Chinese to buy American products. The chart below shows that the US trade deficit with China has stabilized as a result of a strengthening yuan. Exports from China to the US have risen only about 30% since the financial crisis, while exports from the US to China have risen about 133%.

(click to enlarge)

Take a walk through Walmart and you will see that Walmart has already begun diversifying away from Chinese yuan exposure. Before the Chinese began strengthening their currency around 2007, Walmart stores in the US sold very little food. The stores carried mostly Chinese made products. After the yuan strengthened a bit, Walmart began converting its stores into 'supercenters' that stocked more food. The food comes mostly from America. In the latest development, Walmart has begun building stores that sell nothing but food called Walmart Markets. These stores have very few products imported from China.

Mexico is the Future of Manufacturing

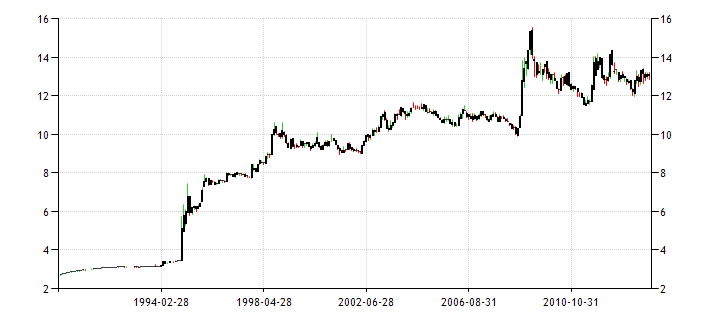

So now that we can see that growth in China is likely to decelerate dramatically, where will that growth go? Some of it obviously has to go to the US, just to keep the US economy remotely stable, but due to NAFTA, Mexico will scoop up most of the most intense early growth. Mexico has lower wages than the US and has more room to lower interest rates if necessary. Mexico lowered interest rates in October. This is at the same exact time that QE is no longer expanding in the US, and is likely to be scaled back over the next year. All of this strengthens the argument that most manufacturing jobs that do move will likely move from China to Mexico, rather than China to the US. The chart below shows that the Mexican peso has weakened dramatically against the dollar since 1990, almost 80%, and the peso is down 2.44% against the dollar over the past year. In other words, the Chinese yuan has strengthened 34% against the dollar since the revaluation began in 2006, but over the same time, the peso has weakened 20% against the dollar. This means the yuan is 54% stronger against the peso just over the past seven years. The result will be greatly decreasing exports from China to Mexico and increased exports from Mexico to China.

(click to enlarge)

The weakened currency over the past several decades in Southeast Asia brought tremendous change to the Chinese government, causing it to become much more capitalist and less communist in nature. International capital flows are already starting to cause major changes in Mexico. The Mexican government has begun recognizing its potential as a world export leader and has started making serious progress in derailing drug cartel power, especially in export sensitive areas such as around seaports. Further evidence of manufacturing growth in Mexico, far and away above that of the US, is that the US has been experiencing a net loss of Mexicans back to Mexico for the past several years. Additionally, manufacturing plants of notable size have been popping up in Mexico. Nissan recently opened the largest car plant in Mexico, and Honda, Mazda, and Volkswagen all have plans to open large plants over the next two years. Mexico also has the advantage of being adjacent to the US, the largest export market in the world.

So now that it is fairly clear that Mexico may eventually overtake China as the world leader in growth, what specific trades should be undertaken to benefit from this?

Recommended Positions:

Because of the likely growth in Mexico, I have a long position in (EWW), the ishares Mexican equity ETF. I also expect China's growth to decelerate, but hold up. Because investors are usually very forward-looking, I am short (FXI), the ishares China equity ETF. I also think US long term government interest rates are likely to rise slightly over the next year, so I have a short position in (TLT), the ishares high duration government bond ETF. If you still want some exposure to the likely mild revival to US car manufacturing, you might want to grab a name like (AXL), a small-cap Detroit-headquartered axle and drivetrain manufacturer with a PE ratio of below 4X and positive earnings for as far out as analysts can see.

Additional disclosure: All of my relevant positions are stated in this article.

No comments:

Post a Comment